Personal loan calculator: Apply in 3min | Response within 24h

Car Loan

Car loans in Luxembourg: understand, compare and act efficiently

Between the variety of financing options available, the need to act quickly in a competitive market and the administrative requirements involved, car loan can play a key role in successfully purchasing a vehicle in Luxembourg.

| Legal requirement | What it means for you |

|---|---|

| Creditworthiness assessment | The lender must verify your repayment capacity before granting the loan in order to prevent over-indebtedness. |

| Pre-contractual information (SECCI) | Before signing, you receive a standardised information sheet detailing the amount, APR, total cost, duration and repayment terms. |

| Withdrawal period (14 days) | You have a legal withdrawal period of 14 calendar days during which you may cancel the agreement without justification. |

| APR transparency | The APR includes mandatory credit-related costs, allowing you to understand the real cost of the loan. |

Whether you are buying a new or used vehicle — a car, motorcycle or motorhome — the right financing solution is one that allows you to act at the right time, with a clear structure, controlled costs and quick implementation.

How does car financing work in Luxembourg?

A car loan is a form of consumer credit used to finance the purchase of a vehicle: car, motorcycle, motorhome or other motorised vehicle. In Luxembourg, its structure follows clear rules and parameters that allow borrowers to understand exactly what they are committing to.

Key components of a car loan

A car loan in Luxembourg is generally structured around three main elements:

- The loan amount: This corresponds to the price of the vehicle, potentially reduced by a personal contribution. It represents the amount effectively financed by the loan.

- The loan term: Expressed in months (for example 120-month or 60-month car loans), it determines the repayment schedule. The longer the term, the lower the monthly instalments — but the higher the total cost of the credit.

- Monthly instalments: These are the amounts repaid each month. They are usually fixed throughout the loan term, providing clear budget visibility.

In addition to these elements, the APR (Annual Percentage Rate) is the key indicator used to compare car loan offers in Luxembourg. It includes not only the interest rate but also all mandatory costs related to the loan. It is therefore the most reliable figure for assessing the true cost of car loan.

Purpose-linked car loan or personal loan?

In practice, car financing in Luxembourg generally takes one of two forms:

- A purpose-linked car loan

- A standard personal loan

| Comparison point | Purpose-linked car loan | Personal loan |

|---|---|---|

| Link with the purchase | Directly linked to the vehicle being financed | Not linked to a specific purchase |

| Proof of purchase | Required (order form or invoice) | Not required |

| Flexibility of use | Use strictly limited to the vehicle purchase | Funds can be used freely |

In both cases, the underlying structure remains the same: a loan amount, a repayment term, fixed monthly instalments and an APR clearly defined at the time of signing.

What are the steps to apply for a car loan?

Applying for a car loan in Luxembourg is generally straightforward when properly prepared.

- Define your project and budget: Before starting the process, it is important to determine the type of vehicle you wish to finance, the maximum budget you are willing to allocate and the monthly payment compatible with your financial situation.

- Run a loan simulation: A car loan simulation allows you to quickly estimate monthly payments, the possible repayment term and the overall cost of the financing. This step helps structure your project and is free and non-binding.

- Prepare your application: A car loan application requires an assessment of the borrower’s financial situation. The documents requested typically include proof of income, current financial commitments and information about the vehicle being financed.

- Application review and preliminary decision: Once the application has been submitted, the lender or broker analyses the request. At Crefilux, car loan applications are reviewed quickly so buyers can secure their purchase without unnecessary delays — particularly when the vehicle they want may be sold quickly.

- Loan approval and disbursement: After approval, the car loan is formalised and the funds are released according to the agreed terms. The borrower then repays the loan through fixed monthly instalments until the end of the term.

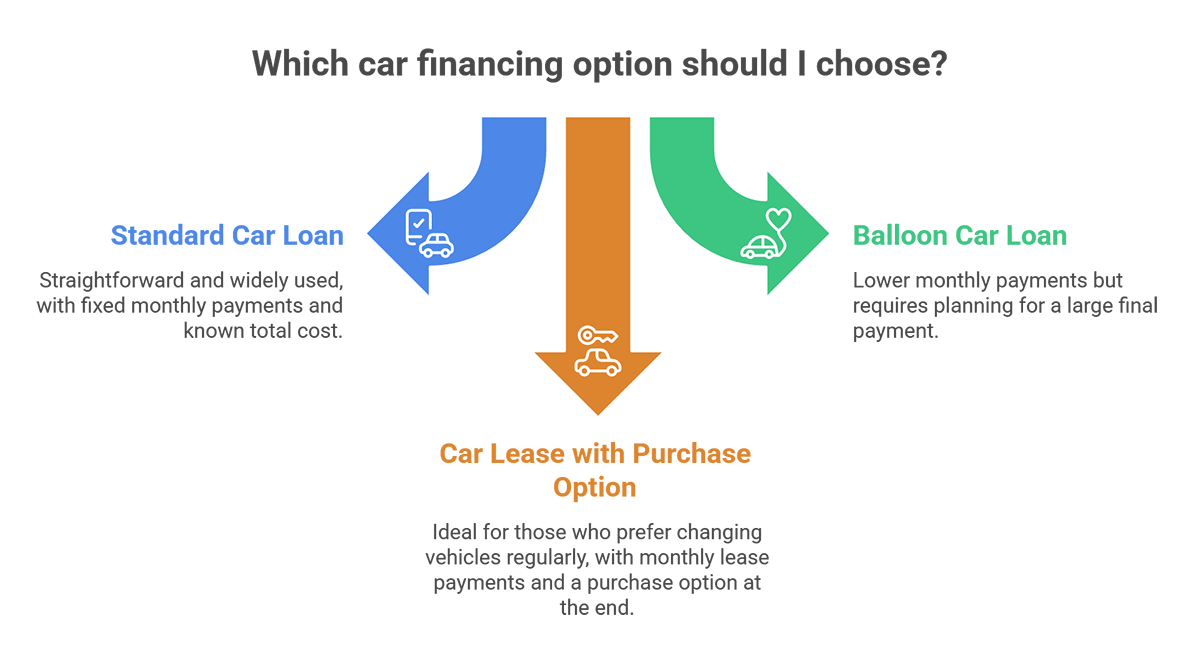

Financing a car in Luxembourg: how does it work?

Standard car loan (personal loan)

With a standard car loan, the buyer immediately becomes the owner of the vehicle. Monthly payments are fixed and the total cost of the loan is known from the start.

This is the most straightforward and widely used financing option, and the one estimated by the car loan calculator at the top of this page.

Balloon car loan

A balloon car loan works similarly to a traditional car loan, but with one key difference.

During the loan term, the borrower makes lower monthly payments because the loan is deliberately under-amortised. At the end of the contract, a significant amount remains to be paid in a single payment. This remaining amount is called the balloon payment.

When the contract reaches its end, three options are generally available:

- Pay the remaining amount using your own funds

- Refinance the remaining balance with a new loan

- Sell the vehicle in order to repay the outstanding amount

A balloon loan can therefore be an interesting way to finance a car in Luxembourg if you want lower monthly payments in the short term. However, it requires planning from the outset how the final payment will be handled.

Car lease with purchase option

A car lease with purchase option does not work like a traditional car loan in Luxembourg. Instead of financing the purchase of the vehicle, you finance its use for a fixed period.

In practical terms, the vehicle is leased for a predefined duration. Each month you pay a lease payment, not a loan instalment. During the entire contract period, the vehicle does not belong to you — it remains the property of the financing organisation.

At the end of the contract, you have two options:

- Return the vehicle

- Purchase it by paying a predetermined amount known as the purchase option

This type of vehicle financing may suit people who prefer changing vehicles regularly and prioritise usage rather than ownership. However, it is less suitable if you intend to keep your vehicle long-term or prefer to avoid contractual constraints.

Comparatif des solutions de financement d’auto

| Solution | Main advantage | Point to consider |

|---|---|---|

| Standard car loan | Simplicity, known total cost | — |

| Balloon car loan | Lower monthly payments | Large final payment |

| Lease with purchase option | Flexibility of use | Contractual constraints |

👉 In summary:

- A standard car loan prioritises simplicity and long-term visibility.

- A balloon car loan reduces monthly payments but requires planning for the final payment.

- A car lease with purchase option offers flexibility but involves stronger contractual constraints.

New or used vehicle: a question of financing… and timing

Choosing between a new or used vehicle is not only a matter of budget. It also directly affects how car loan is structured and how much flexibility the buyer has when applying for a loan.

Financing a new vehicle: a simpler and more predictable framework

Purchasing a new vehicle usually takes place in a well-defined context: the price is known in advance, the seller is a professional dealer and the timeline is often longer (order, delivery). In this situation, the vehicle financing can be arranged in advance without particular urgency.

The car loan is generally structured based on:

- a clearly defined price

- a predictable timeline

- and a purchase project that is unlikely to change in the short term

This allows the buyer to take the time to compare financing options, choose the most suitable loan term and finalise the financing even before the vehicle is delivered.

Financing a used vehicle: more variables and greater time pressure

By contrast, purchasing a used vehicle is often driven by opportunity. The price may be attractive, but the vehicle is usually available immediately and may be sold quickly.

The vehicle’s age, mileage, rarity and the type of seller (dealer or private individual) all come into play. These factors influence not only the choice of vehicle but also how the car loan needs to be arranged.

In this situation, timing becomes a key factor: car financing must often be approved quickly so the buyer can secure the purchase without delay. A lender that takes too long to respond may simply cause the buyer to miss a good opportunity.

Plan your financing according to your purchase project

In practice:

- A new vehicle allows for a more planned and structured financing approach.

- A used vehicle often requires faster financing that can keep pace with the market.

Understanding this difference helps you adapt your financing strategy and avoid delays at a crucial moment.

Electric and hybrid vehicles: combining public subsidies and financing wisely

In Luxembourg, purchasing an electric vehicle — and in some cases a plug-in hybrid — may qualify for public subsidies in the form of grants, which are paid after the purchase if certain conditions are met. From a budgeting perspective, these subsidies reduce the net price of the vehicle and therefore the amount that needs to be financed.

Rather than using personal savings, a balanced approach can be to:

- use public subsidies as the first lever to reduce the overall cost,

- then complement the remaining amount with a car loan.

In this context, the car loan serves a specific purpose: to adjust the financing rather than replace personal savings. By reducing the borrowed amount thanks to subsidies, it becomes possible to shorten the loan term or lower the monthly payments while maintaining a sound financial structure.

This combination of financial resources helps reduce the overall cost of the project without weakening household cash flow — an approach that is particularly relevant for a vehicle considered as a long-term investment.

Motorcycles, motorhomes and vans: financing leisure vehicles

Car financing in Luxembourg is not limited to purchasing a car. It can also be used for many leisure vehicles, whose purchase price can represent a significant financial commitment.

This is particularly the case for:

- Motorcycles, through a motorcycle loan in Luxembourg

- Travel vehicles, financed with a motorhome or campervan loan

- Converted vans, for those looking for a simpler travel setup

Different vehicles, similar financing principles

Whether it is a two-wheeler, a leisure vehicle or a travel project, the underlying situation is often the same: the purchase price can be high and concentrated in a short period of time. Few households wish — or are able — to commit such a large amount immediately.

A loan for a leisure vehicle therefore makes it possible to spread this expense over time, with a loan term and monthly payments adapted to how the vehicle will actually be used, whether occasionally or more regularly.

FAQ: Car loans and vehicle financing in Luxembourg

Can I finance a vehicle purchased abroad?

A car loan can finance this type of purchase, provided the administrative steps are anticipated — particularly insurance and vehicle registration in Luxembourg. Proper coordination helps avoid delays between the purchase and the vehicle being put on the road.

Please note: at Crefilux, loans are intended for Luxembourg residents. However, alternative car financing solutions may also be available for Belgian cross-border workers.

Is a down payment required for a car loan?

A down payment is not mandatory. It can help reduce the loan amount or shorten the loan term, but it is not always the best option.

In some cases, keeping part of your savings while completing the purchase with a car loan may be a more balanced approach. The best solution depends on the buyer’s overall financial situation.

What happens if I sell the vehicle before the loan ends?

It is entirely possible to sell a vehicle before the end of the loan.

In that case, the car loan must be repaid, usually using the proceeds from the sale. A well-structured loan typically allows for this situation through early repayment options included in the contract.

Can I apply for a car loan online after running a simulation?

Yes. After using the simulator, you can continue the process through the associated application form and submit a car loan request online.

This step allows you to provide the initial information required for the analysis of your application. It does not constitute a final commitment but initiates a personalised review by a Crefilux advisor.

The objective is twofold:

- Speed, thanks to the online process

- Human guidance, which remains essential to secure the car loan and adapt it to the borrower’s real situation.

Car loan brokers: speed, expertise and local support

In the Luxembourg car market, a good opportunity is not judged solely by the price or the interest rate. Very often, success depends on the ability to act quickly with financing that is clear and immediately available.

This is where an experienced broker such as Crefilux comes into play.

A team familiar with the realities of the car financing market

At Crefilux, the objective is not only to compare offers but also to make car financing operational quickly.

Thanks to a detailed understanding of the market and the criteria used by our partner lenders, a response can generally be provided within 24 hours. This allows buyers to move forward without delay when timing is critical.

This speed is not achieved at the expense of the client. It relies on a structured analysis carried out by advisors experienced in car financing applications, whether for cars, motorcycles or leisure vehicles.

Expertise rooted in the Luxembourg market

Car loan is not handled the same way everywhere. Market specificities, borrower profiles and the pace of transactions all play a role — and local experience makes a real difference.

With three local agencies in Luxembourg City, Esch-sur-Alzette and Ettelbruck, Crefilux combines:

- Online tools that allow you to move quickly

- Human guidance that remains accessible and responsive

This way, you can choose the level of contact that suits you best while still benefiting from personalised support at every stage.