Debt consolidation calculator: Apply in 3min | Response within 24h

Debt consolidation

Debt consolidation is commonly used to simplify multiple loan repayments or to reduce monthly payments and free up room in your budget. However, it is important to understand that consolidation is neither a “reset” of your debts nor a miracle solution. It is a financial restructuring tool that should be fully understood before you decide to use it.

The aim of this guide is to help you understand how debt consolidation works, in which situations it may be useful, and how to analyse an offer before committing.

What is debt consolidation?

Debt consolidation — sometimes also referred to as loan restructuring or debt restructuring — consists of replacing several existing loans with a single new loan, with one monthly repayment and a new repayment term.

The lender handling the consolidation repays your existing loans directly to your current creditors, and then sets up a new single loan that you repay instead.

In practice, the process usually works as follows:

- The outstanding balances of your current loans are identified;

- The debt consolidation provider repays the lenders concerned directly;

- A new single loan is created with one monthly repayment.

If an additional amount is included in the operation (for example to finance a project or repay an overdraft), the remaining funds may be paid into your account once the previous loans have been settled by the new lender.

Debt consolidation therefore allows you to:

- Replace several monthly payments with one single repayment;

- Adjust the monthly repayment to fit the household budget;

- Make repayments easier to manage.

However, it should not be confused with a cancellation or reduction of debt: the amounts still owed are simply combined and reorganised into a new loan.

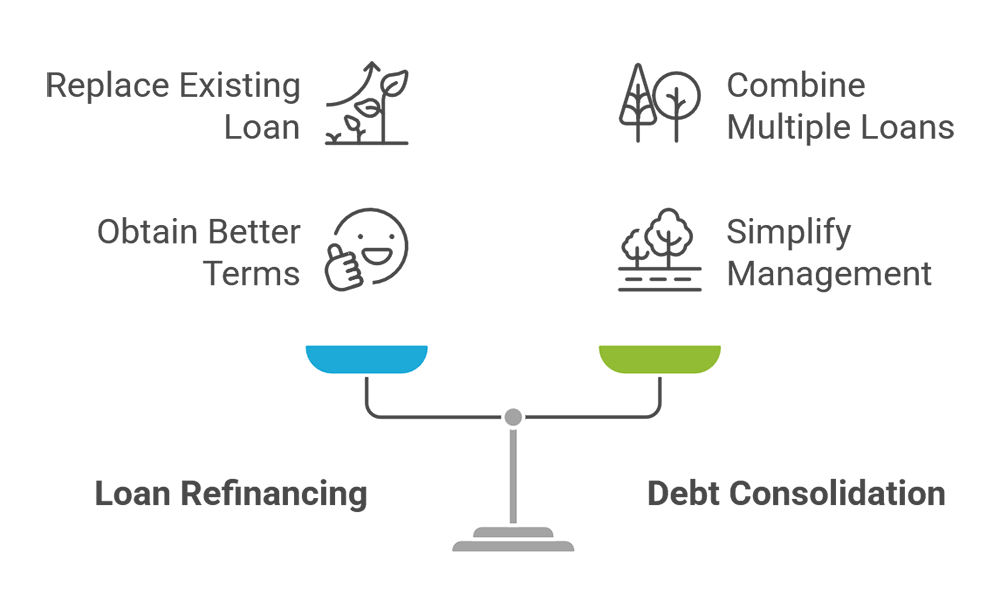

Debt consolidation and loan refinancing: two often confused concepts

The terms debt consolidation and loan refinancing are often used interchangeably, but they actually refer to slightly different financial arrangements.

| Operation | Principle | Main objective |

|---|---|---|

| Loan refinancing | Replace an existing loan with a new one | Obtain better terms (rate, duration, monthly repayment) |

| Debt consolidation | Combine several loans into one | Simplify management and adjust monthly repayments |

A practical example:

- If you only have a car loan and wish to renegotiate its conditions, this is usually considered loan refinancing.

- If you have a car loan, a personal loan and a revolving credit line, and you want to combine them into a single monthly payment, this is considered debt consolidation.

Which loans can be included in debt consolidation?

Depending on the consolidation provider and the borrower’s situation, several types of loans can generally be included in a debt consolidation or debt restructuring operation.

| Type of loan | Can usually be consolidated |

|---|---|

| Personal loan | Yes |

| Car or motorcycle loan | Yes |

| Home improvement loan | Yes |

| Revolving credit / credit line | Yes |

| Bank overdraft | Sometimes |

| Other personal debts | Case-by-case basis |

Revolving credit and credit lines are particularly relevant for this type of operation. Their structure can sometimes lead to very long repayment periods when only the minimum payment is made. Consolidating these debts helps clarify the real repayment timeline and permanently close these credit lines.

However, the possibility of including certain debts in a consolidation depends on several factors:

- The terms of the existing contracts;

- The remaining balances to be repaid;

- The borrower’s financial situation.

When in doubt, it is usually necessary to review the existing loan agreements to determine what should realistically be included in the consolidation. If needed, you can contact one of our advisors for guidance.

Advantages and limitations of debt consolidation

The table below summarises the main possible effects of debt consolidation:

| Potential benefit | Trade-off to consider | When it may be relevant |

|---|---|---|

| Lower total monthly repayments | Repayment period is often longer | When current monthly payments are putting too much pressure on the budget |

| A single monthly payment to manage | The loan may last longer | When multiple loans make financial management complicated |

| A clearer view of your financial situation | The overall cost of the credit may be higher | When the main objective is to stabilise the budget |

| Possibility to include additional cash | Risk of re-borrowing if the budget is not well managed | When the additional funds are used for a clearly defined project |

| Overall restructuring of existing debts | Some fees may apply depending on contracts (e.g. early repayment fees) | When several loans have accumulated over time |

The principle behind debt consolidation is a balance between monthly repayment, loan duration and total cost. The key question is therefore: what is your main objective? What priority should the debt consolidation fulfil for you?

Example & simulation of debt consolidation

To better understand how debt consolidation works, it can be useful to look at a concrete example. Please note that the goal here is not to represent every possible situation or real market figures. This example is provided for illustrative purposes only.

Scenario

Let us imagine a borrower (Mr Schmitt) who is currently repaying three different loans taken out at different times.

| Loan | Outstanding balance | Monthly repayment | Remaining term |

|---|---|---|---|

| Personal loan | €8,000 | €190 | 48 months |

| Car loan | €12,000 | €320 | 42 months |

| Revolving credit | €3,000 | €90 | Variable |

| Total | €23,000 | €600 | — |

In this situation:

- Three loans are being repaid simultaneously;

- The total monthly repayment amounts to €600;

- Each loan has different terms and repayment conditions.

Mr Schmitt’s main objective is to reduce the pressure on his monthly budget. He therefore submits a debt consolidation request online.

Comparison before and after debt consolidation

After reviewing the application, a lender proposes the following debt consolidation structure:

| Situation | Total monthly repayment | Duration | Number of loans |

|---|---|---|---|

| Before consolidation | €600 | Different maturities | 3 |

| After consolidation | €360 | 84 months | 1 |

With this new single loan, Mr Schmitt’s situation becomes:

- The three loans are replaced by one consolidated loan;

- The monthly repayment decreases from €600 to €360;

- The repayment period is extended in order to reduce the monthly payment.

Mr Schmitt has therefore achieved his objective. His debt consolidation has allowed him to lower his monthly repayments and reduce the pressure on his budget. However, it is important to remember that consolidation always involves trade-offs depending on your main objective:

- Monthly repayments can be significantly reduced when the repayment period is extended;

- Several loan contracts are replaced by a single monthly repayment;

- The new repayment term may be longer than the original loans.

Avoiding pitfalls: when is debt consolidation less appropriate?

Beyond purely numerical criteria, other factors should also be considered to determine the most suitable debt consolidation solution for your situation. When several loans are already in place, it is not always advisable to consolidate all of them automatically. In some cases, partial debt consolidation may be more appropriate than a full consolidation. This approach involves consolidating only part of the existing loans, while leaving aside those that may be more advantageous to keep unchanged.

This may be the case, for example, when:

- one of the loans is close to its final repayment;

- some loans already benefit from particularly favourable conditions;

- a full debt consolidation would significantly extend the repayment period (the acceptable threshold will depend on your financial situation and objectives).

In other words, the best consolidation strategy is not necessarily the one that includes every existing loan, but the one that genuinely improves the balance of your budget without unnecessarily worsening the repayment terms.

How is debt consolidation calculated?

Before looking at how debt consolidation is calculated, it is useful to understand a few key concepts. These terms appear systematically in simulations and financing proposals.

Understanding them will help you read and compare debt consolidation offers more effectively.

| Term | Definition | Where to find it |

|---|---|---|

| Outstanding balance (remaining principal) | The amount that still needs to be repaid on a loan at a given moment. | Amortisation schedule or loan statement |

| Monthly repayment | The amount repaid each month. It includes both principal and interest. | Loan agreement or bank statements |

| Remaining term | The number of months left before an existing loan is fully repaid. | Contract or amortisation schedule |

| APR (Annual Percentage Rate) | Indicator representing the total cost of the loan. It includes the interest rate and associated fees. | Credit offer or loan simulation |

| Early repayment fees | Fees that may apply when a loan is repaid before its original term. | Terms of the loan agreement |

| Borrower insurance | Insurance covering certain risks (death, disability, inability to work). | Insurance contract or loan offer |

| Additional cash | An amount added to the consolidation to finance a project or cover an expense. | Determined during the application review |

| Repayment capacity | The portion of income that a borrower can allocate to loan repayments. | Income, expenses and budget analysis |

Calculating debt consolidation in three steps

Once these elements are gathered, debt consolidation is generally structured in three stages:

| Step | What is done | Purpose |

|---|---|---|

| 1. Calculating the total amount to refinance | The outstanding balances of the existing loans are added together. Early repayment fees and any additional cash requested may also be included. | Determine the amount of the new single loan that will replace the existing loans. |

| 2. Determining an appropriate repayment term | The lender reviews the borrower’s income, expenses and repayment capacity. The duration of the new loan is adjusted accordingly. | Find a balance between the monthly repayment and the loan term so that repayments remain compatible with the household budget. |

| 3. Calculating the new monthly repayment | Once the amount and duration are defined, the lender calculates the monthly repayment, the APR and the total cost of the financing. | Compare the situation before and after consolidation and evaluate whether the operation is relevant. |

Among the qualitative aspects of a debt consolidation agreement, it can also be useful to check the flexibility of the contract. Some loan agreements allow early repayment or adjustments to the monthly instalments during the repayment period, which can provide valuable flexibility over time.

Debt consolidation in Luxembourg: legal framework and borrower rights

Like any consumer credit operation, debt consolidation in Luxembourg is governed by rules designed to protect borrowers and ensure transparency in the offers provided.

Receiving clear information before signing

Before signing a debt consolidation agreement in Luxembourg, the lender must provide the borrower with detailed information about the financing conditions.

These mandatory disclosures include the key elements of the offer:

- the amount of credit proposed;

- the APR (Annual Percentage Rate);

- the repayment period;

- the amount of the monthly repayments;

- the total cost of the credit.

Transparency requirements for credit intermediaries

When a broker proposes a debt consolidation solution in Luxembourg, they must also comply with transparency obligations. In particular, they must:

- explain their role in the operation;

- specify the nature of their remuneration;

- provide clear and understandable information about the proposed financing conditions.

The right of withdrawal after signing

Debt consolidation in Luxembourg is subject to a 14-day withdrawal period. This means the borrower may cancel the agreement within 14 days of signing the contract, without having to provide any justification.

What to do in case of a dispute or question?

If a disagreement arises with a financial institution or credit intermediary, you can file a complaint or use mediation procedures. In Luxembourg, the Commission de Surveillance du Secteur Financier (CSSF) supervises financial institutions and may intervene in certain dispute situations.

To learn more about borrower rights and available procedures, you can consult the official information available on Luxembourg public websites, including:

- lu, which explains the rules applicable to consumer credit (and therefore also to consumer debt consolidation);

- The CSSF, which provides information on complaint procedures and consumer protection.

Consolidating your debts with Crefilux: a structured approach

At Crefilux, our approach is simple and structured.

Note: Some situations require a faster response. Thanks to its internal processes and established relationships with financial partners, Crefilux can provide very fast debt consolidation solutions when necessary.

A professional review of your financial situation

The first step is to examine the key elements that help determine whether debt consolidation is appropriate:

- the outstanding balances of each existing loan;

- the current monthly repayments;

- the household’s income and expenses;

- any need for additional cash.

This analysis helps determine whether the operation is suitable for your situation and, if so, on what basis it can be structured.

Finding a suitable debt restructuring solution

Once the application has been reviewed, Crefilux searches for the most appropriate debt consolidation solution and competitive terms for your situation.

This stage involves:

- identifying financial partners likely to accept the application;

- comparing the proposed conditions (monthly repayment, duration, total cost, insurance);

- reviewing the important contractual elements before any decision is made.

This approach allows you to understand the available options without having to contact multiple lenders individually.

Preparing and reviewing the application

Setting up a debt consolidation usually requires several supporting documents, such as:

- identity documents;

- proof of income;

- recent bank statements;

- contracts or statements relating to existing loans;

- early repayment statements when necessary.

Crefilux verifies that the application is complete and consistent with the requirements of its financial partners, helping to facilitate the review process and avoid unnecessary delays.

Get an initial estimate of your debt consolidation

Since every financial situation is different, the best way to assess the relevance of debt consolidation is to run an online simulation. You can use the Crefilux debt consolidation simulator to test different parameters and estimate possible outcomes.

If you would like to go further, or if you have any doubts, you can contact a Crefilux advisor directly. They will review your situation and guide you towards the most suitable solutions available.