Loan refinancing simulator: Apply in 3min | Response within 24h

Loan refinancing

Loan refinancing: how to reduce your repayments and save money

Loan refinancing can help optimise your loan and ease pressure on your finances. Conversely to common belief, it is not a last-resort solution. Instead, it is a practical way to renegotiate the terms of an existing loan. Whether your goal is to reduce your monthly repayments or shorten the repayment period, refinancing a loan can help you adjust your budget to match your current financial objectives, while potentially benefiting from more favourable market interest rates. Discover how this financial strategy can help you save money without significantly disrupting your finances.

In brief: loan refinancing

- Definition: a solution that allows you to refinance a single loan, either reducing monthly repayments or shortening the loan term.

- Difference from debt consolidation: refinancing improves the terms of a single loan, whereas debt consolidation combines several loans into one.

- Not only for financial difficulties: it can also be useful to benefit from better loan conditions even when there are no financial problems.

- Requirements in Luxembourg: lenders generally expect stable employment, a reasonable debt ratio and a good credit history.

- Insurance and risks: although optional, insurance can help secure repayments in case of unforeseen events. It is important to consider associated costs to ensure the operation remains financially worthwhile.

- Running a simulation: essential to compare offers and estimate potential savings.

What is loan refinancing?

Loan refinancing is a solution that allows you to reduce your monthly repayments or shorten the repayment period of an existing loan by renegotiating its terms. Unlike debt consolidation, refinancing concerns a single loan that you refinance at potentially more favourable conditions.

One of the main advantages of loan refinancing is that it can lower your monthly repayments or shorten the repayment period. It is particularly relevant when interest rates have decreased since you originally took out your loan.

This process can be carried out with your current bank or with another financial institution offering more attractive refinancing conditions. By doing so, you adjust your repayment plan to your current financial situation, which may provide greater flexibility for your budget.

Loan refinancing and debt consolidation: are they the same thing?

Although loan refinancing and debt consolidation are often used interchangeably, there is an important distinction between the two.

Loan refinancing consists of refinancing one existing loan under more favourable conditions. The goal is typically to reduce the monthly repayment or shorten the remaining loan term, allowing the borrower to achieve financial savings. In this sense, refinancing is primarily focused on optimising the cost of a single loan.

Debt consolidation, on the other hand, involves refinancing several loans (at least two) and combining them into a single new loan. The main objective is to reduce the overall monthly repayment burden, since the borrower only has one repayment to manage. This often results in a longer repayment period than the original loans but simplifies financial management.

In short: Loan refinancing focuses on financial savings on a single loan. Debt consolidation focuses on simplifying repayment and easing the monthly burden.

Mini-FAQ: Loan refinancing

Is loan refinancing only for people in debt?

Not at all. Contrary to common belief, loan refinancing is not limited to situations of financial difficulty. It can be useful for many borrowers, even when their financial situation is stable. For example, some people choose to refinance a loan to benefit from better repayment conditions, reduce their monthly payments or adjust the loan term according to their current financial situation.

In other words, loan refinancing can be a flexible financial management strategy, not simply a last-resort solution.

Can you refinance only one of your loans?

Yes. Unlike debt consolidation, which combines several loans into one, loan refinancing typically applies to a single specific loan.

If you wish to optimise the terms of a particular loan — such as a mortgage or a consumer loan — refinancing can be a relevant option. For a detailed evaluation of your refinancing options for a personal loan or another type of credit, you can consult a Crefilux advisor, who will help identify the solution best suited to your financial situation.

What are the requirements for loan refinancing?

In Luxembourg, the requirements for obtaining loan refinancing are broadly similar to those in other countries, although some local specificities may apply. Below are the main criteria typically assessed by Luxembourg financial institutions.

Employment stability

Lenders generally favour borrowers with a stable professional situation, such as a permanent employment contract or a consistent employment history. Stability is seen as an indicator of regular income, reassuring lenders about your ability to meet repayment obligations.

Income level

Your borrowing capacity is closely linked to your income. Financial institutions typically evaluate your debt-to-income ratio, which represents the percentage of your net monthly income used to repay existing debts. Although there is no strict legal threshold, a ratio below 33% is often considered acceptable by lenders.

Credit history

Responsible management of past debts is essential. Late payments or defaults can negatively affect your application. Lenders may consult the Central Bank of Luxembourg’s credit database, and being listed there for repayment incidents may compromise your chances of obtaining a refinancing.

Loan-to-value ratio (LTV)

In the case of mortgage refinancing, lenders often consider the loan-to-value ratio (LTV). This indicator compares the loan amount with the value of the property used as collateral. In simple terms, a lower LTV ratio is generally viewed more favourably by lenders because it indicates a more stable financial position and a lower risk of default.

It is important to note that requirements may vary between financial institutions. For this reason, it is often advisable to compare several offers and discuss your situation with financial advisors to better understand the conditions of each refinancing proposal.

What are the specific features in Luxembourg?

When exploring financial services such as loan refinancing in Luxembourg, it is important to understand that conditions can differ from those in other countries due to local legal and economic factors.

- Financial regulation: Luxembourg, as an international financial centre, operates under strict regulatory oversight that can influence the credit products available, including refinancing solutions. Banks and financial institutions operate under the supervision of the Commission de Surveillance du Secteur Financier (CSSF), which imposes high standards of transparency and solvency.

- Interest rates: Interest rates in Luxembourg may differ from those in other European countries due to the country’s economic structure and financial stability. Rates are often competitive but vary depending on the borrower’s profile and the nature of the credit.

- Loan conditions: Conditions such as loan duration, processing fees and early repayment options may be influenced by local regulations. Some loans offer flexible repayment options without penalties, while others may include stricter contractual restrictions.

- Specialised offers: Given Luxembourg’s international population, banks may offer products specifically designed for expatriates and cross-border workers. These products may include conditions tailored to attract these profiles.

- Expert guidance: Because of these nuances, it is often advisable to consult a local financial expert such as Crefilux, who understands both Luxembourg regulations and the financing options available on the market. An advisor can help you navigate the financial landscape and identify the refinancing solution best suited to your personal situation.

What are the risks of loan refinancing?

When considering loan refinancing, it is important to be aware that certain pitfalls and risks may exist. The terms of the new loan may have long-term implications.

The main risk is that the new loan does not offer truly advantageous conditions. For example, if the interest rate of the new loan is only slightly lower than your current one, or if additional costs apply (such as administrative fees or early repayment penalties), the financial benefit may be limited.

For larger refinancing operations — particularly mortgage refinancing or high loan amounts — the impact can be even more significant. When refinancing a substantial amount, even a small difference in interest rates or fees can have a considerable effect on the overall cost of the loan. Large refinancing operations may also involve additional fees proportional to the loan amount, which can increase the total cost.

It is also important to ensure that the terms of the new loan — such as early repayment conditions or options to renegotiate the loan in the future — are sufficiently flexible to adapt to potential changes in your financial situation. Terms that are too restrictive could lock you into a less flexible loan and make financial management more difficult later on.

Before committing, carefully compare the new loan conditions with those of your current loan. If necessary, seek advice from a financial expert to determine whether refinancing is truly beneficial in your situation.

In which situations can loan refinancing be useful?

Is loan refinancing possible for a business loan, and what are the benefits?

Yes, loan refinancing can also apply to business loans and may be a useful strategy for entrepreneurs or companies seeking to reduce their financial burden. The principle is similar to refinancing for individuals: the goal is to refinance an existing loan under more favourable conditions, often with a lower interest rate or an adjusted repayment period.

Refinancing a business loan can free up financial resources and improve cash flow, allowing the company to invest in growth projects or manage unexpected expenses. For example, if a company took out a loan at a relatively high interest rate and market rates have since decreased, refinancing may reduce monthly repayments and improve available cash flow.

However, before opting for business loan refinancing, it is important to carefully evaluate the associated costs — such as early repayment penalties or administrative fees — and ensure that the new conditions truly provide a long-term financial benefit.

Refinancing a renovation loan: is it a good option?

Refinancing a home improvement loan can be an effective solution if you already have a loan for renovation work and want to reduce its overall cost. By renegotiating this loan at a more favourable interest rate, you may be able to lower your monthly repayments or shorten the repayment period.

This can help you manage your budget more effectively while continuing your renovation projects under more favourable financial conditions.

Loan refinancing after a divorce: how does it work?

After a divorce, loan refinancing can help simplify financial arrangements by transferring a loan into a single borrower’s name, particularly if the original loan was taken jointly.

This option allows you to refinance a mortgage or personal loan under conditions that reflect your new financial situation. Depending on the terms negotiated, this may reduce monthly repayments or adjust the repayment period to better match your current financial capacity.

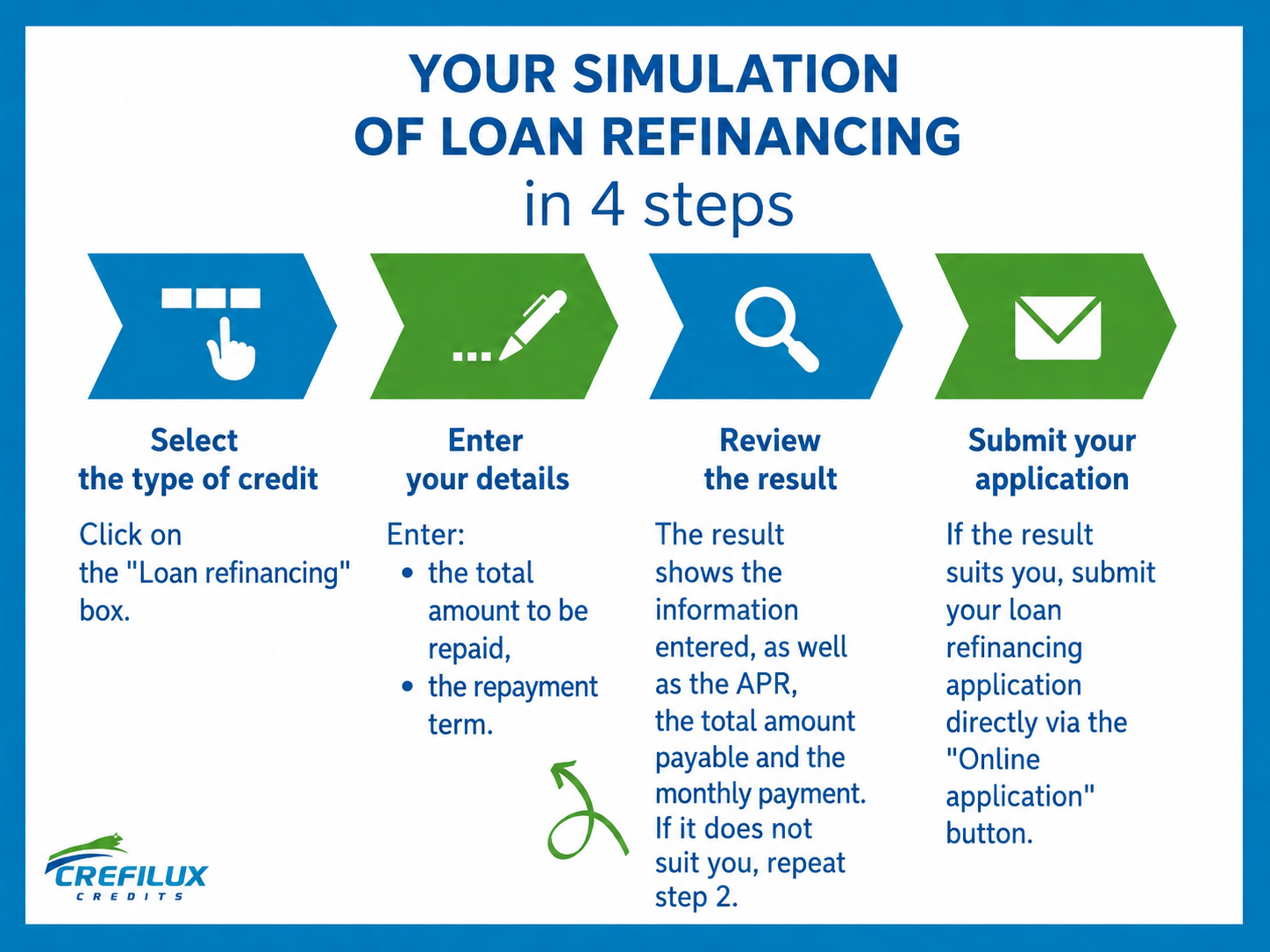

Run a simulation before refinancing your loan

Before committing to loan refinancing, it is highly advisable to run an online simulation (similar to getting an estimate for your refinancing project). This step, which is free with Crefilux, works as a financial preview: it allows you to estimate what your monthly repayments could look like under different refinancing scenarios.

You can think of it like trying on a pair of shoes before buying them — you want to be sure they fit properly. In the same way, a refinancing simulation allows you to preview the potential new loan conditions — the monthly payment, the loan term and the interest rate — to ensure they align with your budget and long-term financial objectives.

Running an online simulation for your refinancing offers several advantages:

- Financial clarity: you gain a clear picture of how your budget may change after refinancing, helping you determine whether the new conditions are genuinely beneficial.

- Comparison: you can compare several offers side by side, which is essential for identifying the most favourable rates and conditions.

- Preparation: it helps you prepare for discussions with lenders, since you already have a realistic idea of what conditions to expect.

Running a simulation before proceeding with loan refinancing online is an important step that helps you make a well-informed decision and avoid unpleasant surprises later. It is a valuable tool for improving your financial planning without any obligation or upfront cost.

Crefilux: your loan refinancing expert in Luxembourg

Are you looking for the best lender for loan refinancing? At Crefilux, we specialise in this field, offering personalised financial solutions to help clients in Luxembourg optimise their existing loans. As specialists in loan refinancing, we develop strategies tailored to the specific needs of each borrower.

Our refinancing process begins with a thorough evaluation of your financial situation in order to identify the most suitable solution. We offer personalised consultations during which our financial advisors guide you through every step of the refinancing process. They help you understand the different options available and identify the refinancing solution that best balances savings and financial stability.

Crefilux is committed to finding loan refinancing solutions with competitive rates and conditions adapted to your situation. We ensure that your refinancing process is handled under the best possible conditions, with continuous support and professional guidance. Take the time to evaluate your options and consult financial professionals — after all, it’s about your finances and your future.

You can also contact us by phone:

- Ettelbruck: +352 268 133 12

- Esch-sur-Alzette: +352 265 323 05

- Windhof: +352 263 053 22